Melbourne’s greenfield growth corridors critical to delivering new homes Victoria - RPM Research

Contact

Melbourne’s greenfield growth corridors critical to delivering new homes Victoria - RPM Research

Melbourne and Geelong’s greenfield growth corridors are critical to delivering much-needed new homes in Victoria, as strong population growth and immigration continue to challenge housing supply, Q4 2023 Victorian Greenfield Market Report from RPM Research, Data & Insights reveals.

-

RPMLuke Kelly RPM National Managing Director Project Marketing

RPMLuke Kelly RPM National Managing Director Project Marketing -

RPMQ4 2023 Victorian Greenfield Market Report from RPM Research, Data & Insights

RPMQ4 2023 Victorian Greenfield Market Report from RPM Research, Data & Insights -

PRMQ4 2023 Victorian Greenfield Market Report from RPM Research, Data & Insights

PRMQ4 2023 Victorian Greenfield Market Report from RPM Research, Data & Insights

Mar 3, 2024

Fresh optimism in Melbourne and Geelong’s new land market, improving economic conditions and a growing population are set to buoy sales in 2024, after transactions fell to an 11-year low in the last quarter of 2023, a new report from RPM Research, Data & Insights shows.

RPM’s latest Q4 2023 Victorian Greenfield Market Report reveals new land sales declined to just 1,770 in the December quarter, 12% below the same period in 2022, and the lowest level since 2012.

Across the year, just 7,839 new lots sold, marking a 46% decline on the previous 12-month period, when 14,602 homesites changed hands.

Despite the fall in sales activity, prices remained stable during quarter four, declining just 0.5% to an average $386,900, while the median lot size shrank 1.1% to 350sqm.

RPM National Managing Director Project Marketing Luke Kelly said while it had been a tough end to the year, buyers had entered 2024 with renewed confidence.

“Purchasers are recognising they are now in the box seat to negotiate a good deal, with the sustained period of constrained sales favouring a buyers’ market,” he said.

“Developers are continuing to offer incentives in the order of five to 10%, saving an average of about $30,000, and the selection of titled lots available means purchasers can have their choice of homesite and start building immediately if they desire.

“The combination of expected rate relief with falling inflation is likely to improve affordability and ease cost-of-living pressures for everyday households.

“The Federal Government’s Stage 3 tax cuts will also put more money back into people’s pockets from July, improving borrowing capacity by four to six per cent, which is good news considering rising interest rates have taken a 30% bite out of purchasing power over the last 18-months or so.

“We saw an uptick in sentiment and sales during the four months to October when interest rates remained on hold. We expect to see that trend again, given the strong start to 2024.”

Mr Kelly said the greenfield market was critical to helping solve Victoria’s housing crisis, with forecast average population growth of 1.7% over the next decade and international immigration, adding about 127,000 new residents to the state each year.

“The greenfield land market is best placed to meet the needs of our growing population and deliver the volume of relatively affordable property needed close to Melbourne CBD and key economic and lifestyle centres,” said.

Mr Kelly said buyers delaying purchasing decisions due to cost of living pressures, particularly in the younger age demographic, was contributing to burgeoning pent-up demand for new

“We’re seeing younger, more price sensitive buyers continue to wait until economic conditions improve, more-so than mature first home buyers, who are generally better equipped to weather the economic environment,” he said.

“As a result, those aged 35 to 54 have taken over as the most predominant first home buyer group, accounting for 43% of sales, compared to 36% for those aged 25 to 34.

“Ever-increasing rental prices will be a catalyst for change, making purchasing property look more attractive to younger buyers.”

First home buyers remained the predominant owner-occupier purchaser of new greenfield land, accounting for 58% of sales, with 70% of those families.

Mr Kelly said slow absorption rates had resulted in developers holding on to new stock, with just 1,452 lots introduced to Melbourne’s growth regions over the past 12 months, a 22% decline.

The average days on market for new land pushed out to more than six months, at 186 days.

“Developers are holding on to new releases in existing communities and delaying the launch of new projects,” said Mr Kelly.

“At the current sales rate, we have about 10 months of stock available, so we’re anticipating new releases won’t start coming to the market until the second half of the year.

“The lots being held back are generally the most sought-after so when new stock is released, prices are anticipated to elevate, so those who are waiting could miss out on buying at today’s prices.

“We’ll likely see Geelong, where sales remain low, take longer to recover, while Melbourne’s other growth corridors are anticipated to rebound faster in both volumes and prices.”

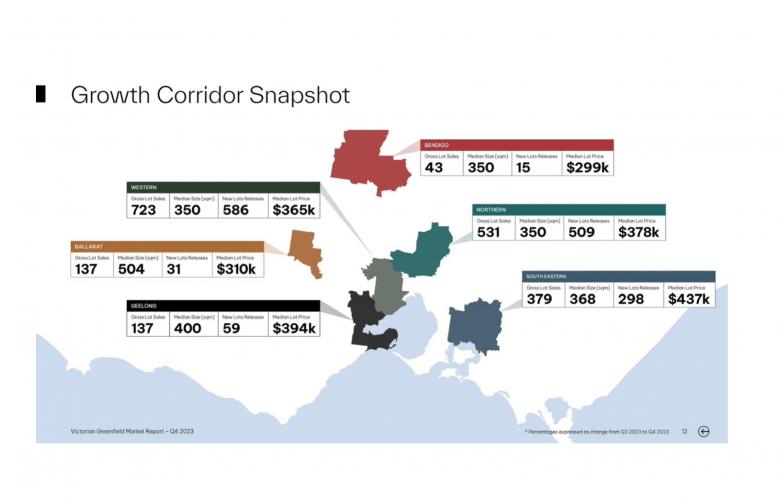

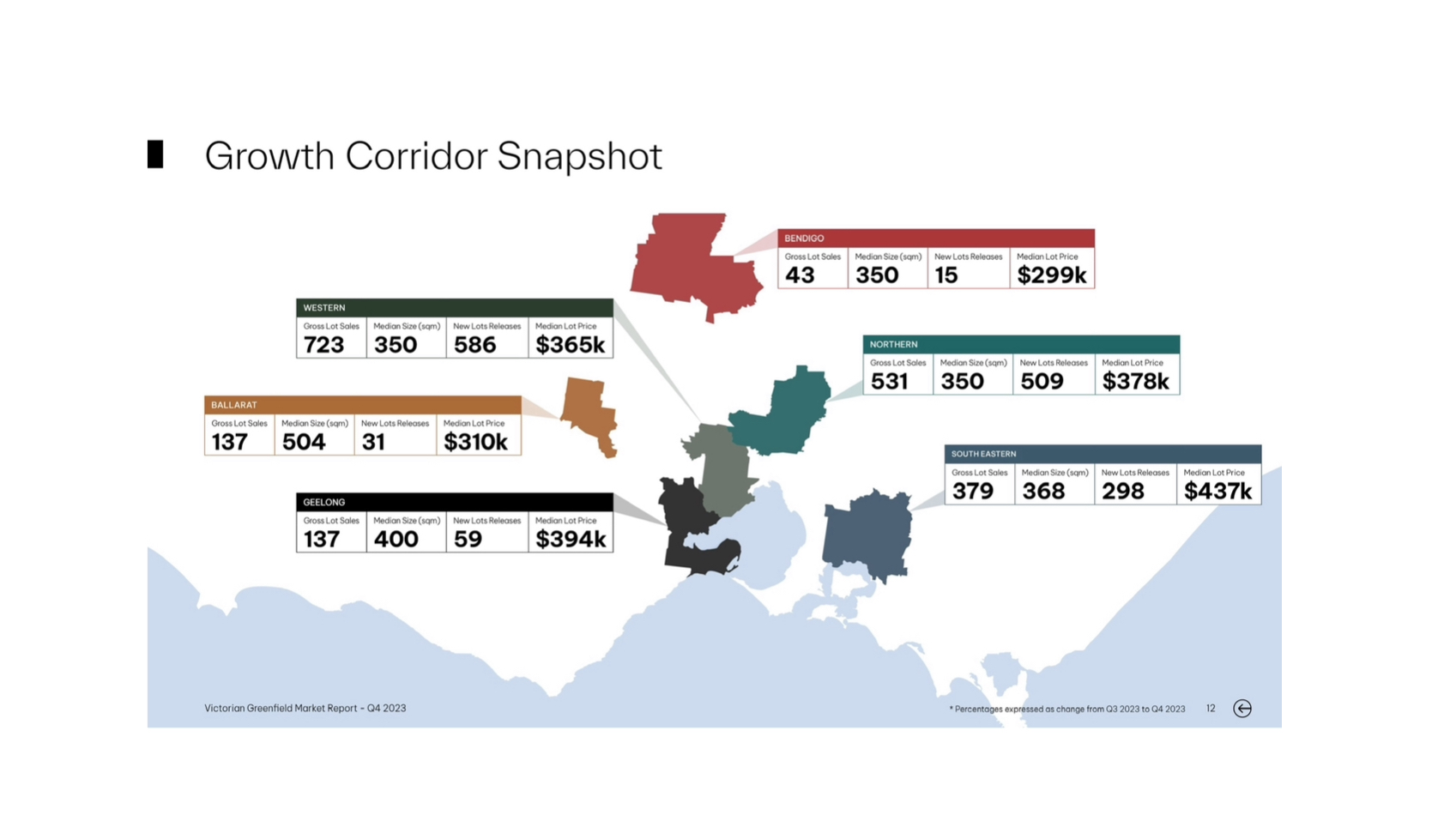

CORRIDOR MARKET ACTIVITY IN Q4 2023:

- The Western Growth Corridor accounted for the lion’s share of sales during the quarter, with 723 new lots changing hands, representing 41% of all land sales in the region. Despite this, there was a modest 5% decline in overall sales. Demand for Melton boosted figures, with sales lifting 10%, making it the only Melbourne area to experience growth during the quarter. The West became Melbourne’s most affordable corridor for the first time since Q2 2019, with the median value declining 5.2% to $365,000. New lot supply reduced by 4%, with 586 new lots released.

- The Northern Growth Corridor lost its position as the most affordable of Melbourne’s four growth regions to the West, with values increasing 2.4% to $378,900, despite a fall in sales.

The 20% dip in sales activity over the quarter saw just 531 lots change hands, with the North accounting for about a third (30%) of all land sales across the growth corridors, a decline on its previous share of 33% but above its long-term average. Among the growth corridors, the North maintained the lowest average time spent on market, with lots taking 113 days to sell. New supply dipped 2% to 509, driven by double-digit growth in Whittlesea and Sunbury, which recorded the strongest increases in lot values at 4.9% and 0.3% respectively.

- The South East Corridor achieved the highest annual growth rate of any of Melbourne’s four growth regions, increasing by 9% in 2023, and 0.6% in the December quarter, to $437,500. Despite the lift, sales continued to decline, dropping 17% to 379 lots, with the fall more pronounced in Cardinia than Casey. The South East contributed to 21% of total sales activity across the four regions. New supply dropped 14% to 298 lots, driven by a 50% reduction in lot releases in Cardinia, contrasting to a 3% increase in Casey. The South East experienced the longest average time on market of the Melbourne corridors, with lots taking approximately six months to sell.

- The Geelong Growth Corridor experienced an improvement in affordability during the quarter, with the median lot value dipping 1.8% to $394,000, on the back of near long-term low sales activity. Just 137 lots changed hands in quarter four, a similar volume to the previous two quarters. Weak demand saw the average lot take more than seven months to sell, marking the longest time on market of all growth corridors. The median lot size remained steady at 400sqm, with the median price per square metre dropping below $1,000. Developers continued to hold new land releases, with just 59 new lots introduced to the market, a 6% decline on last quarter’s decade low.

To read RPM Research, Data & Insights’ full Q4 2023 Victorian Greenfield Market Report, visit RPM Q4 2023 - Victorian Greenfield Market Report by RPM Group - Issuu

Related Reading:

Important Information:

Contact details:

Luke Kelly

RPM National Managing Director Project Marketing

Email

13367

13311

Luke Kelly

Most popular

Our contributors